Since the publication of this article, Docoon has received its temporary registration as a Partner Dematerialization Platform from the Directorate General of Public Finances under number 19.

As part of the electronic invoicing reform, many of the companies we meet and partners we work with are asking the same question: should we choose a Dematerialization Operator (DO) or a Partner Dematerialization Platform (PDP)? Docoon is positioning itself as a future Partner Dematerialization Platform registered and certified by the government. In concrete terms, this means that we have already implemented a dematerialized solution that meets all the standards required by the government to enable our customers to use electronic invoicing from January 1, 2024.

(*) The DGFiP (Directorate General of Public Finances) announced in a press release on July 28, 2023, that the implementation date of the reform had been postponed indefinitely. As part of the 2024 finance bill, the widespread use of electronic invoicing will be implemented in two stages starting in 2026.

The obligation to issue electronic invoices will be implemented:

- September 1, 2026 September1, 2026 for large companies and medium-sized companies (ETI);

- September 1, 2027 September1, 2027 for small and medium-sized enterprises (SMEs) and micro-enterprises.

The obligation to receive electronic invoices will apply to all companies from September1, 2026.

1. OD and PDP: what are they?

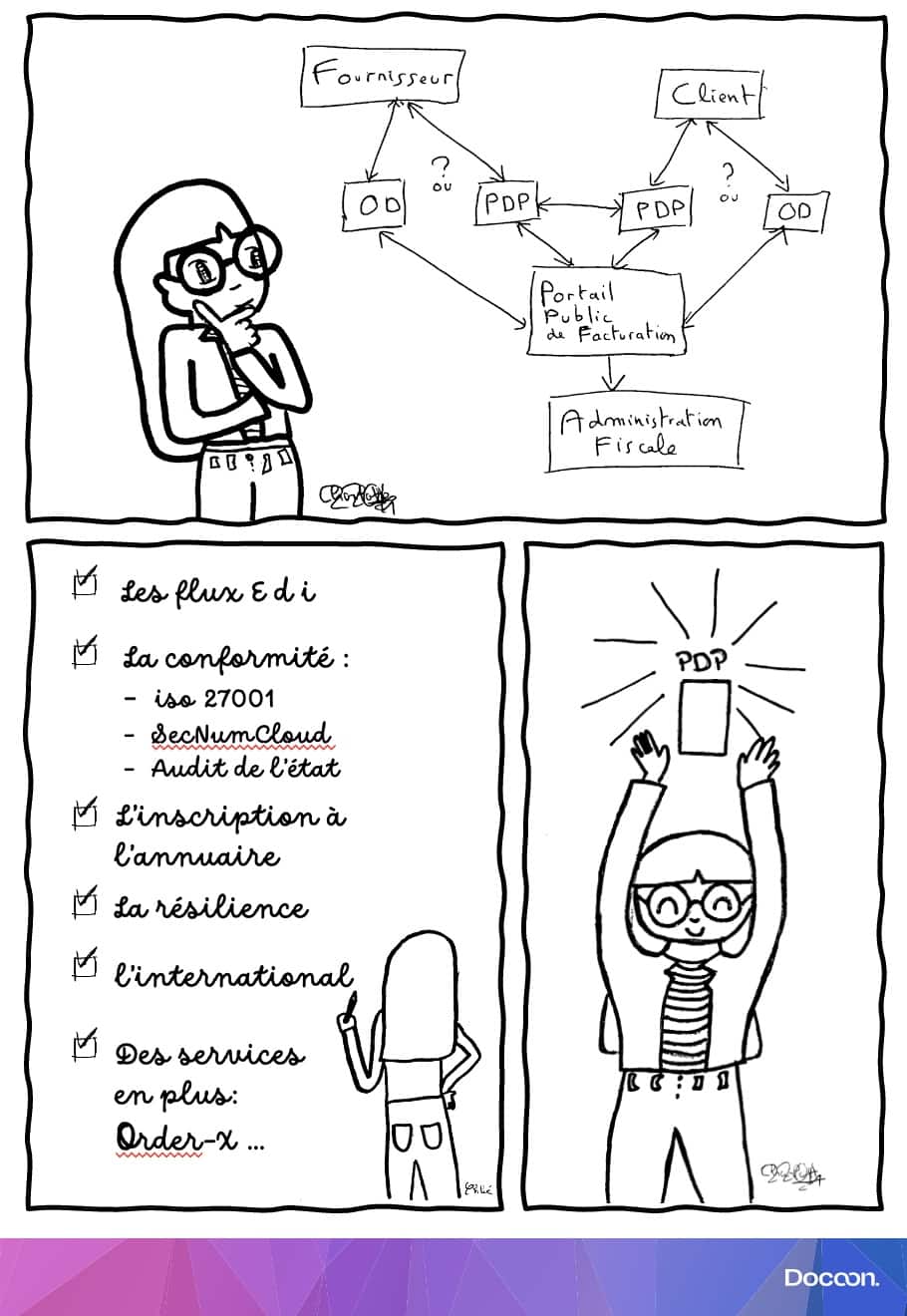

A Dematerialization Operator is an intermediary that connects to the public invoicing portal on behalf of its client to enable them to send/receive invoices, track the invoice lifecycle, and manage e-Reporting. The client of a Dematerialization Operator is required to create an account on the Public Invoicing Portal (PPF) and provide it to the Dematerialization Operator so that the latter can act on their behalf.

Please note: since this article was written, on October 15, 2024, the government announced a significant reduction in the scope of the PPF (Public Invoicing Portal). This public platform, initially designed to issue, receive, and manage electronic invoices for businesses, will now focus solely on two functions: the business directory and the tax data hub for e-reporting. As a result,all companies will now have to turn to a Partner Dematerialization Platform (PDP) to exchange their invoices and report VAT.

What is a Partner Dematerialization Platform (PDP)? As part of the 2024 electronic invoicing requirement, the government has favored a Y-shaped model based on registered and audited platforms (PDPs) for:

- Bringing greater resilience to the system

- Enabling companies to maintain existing flows (EDI flows)

- Promote innovation by allowing operators to offer an alternative to the public billing portal. PDPs will thus be able to offer innovative solutions for identifying and authenticating companies or offering additional services.

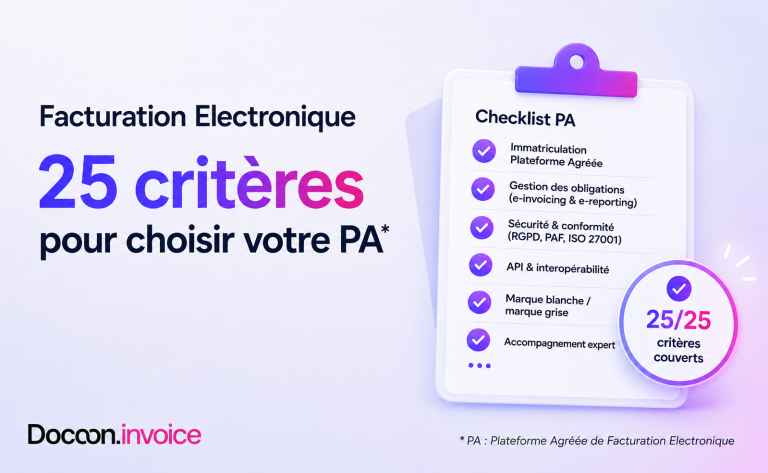

Consequently, a Partner Dematerialization Platform will offer the same services as a Dematerialization Operator, but with certain prerogatives (registration in the official directory, exchange of invoices in formats other than the base format) and very strict specifications: ISO 27001, SecNumCloud hosting, and an obligation to be interoperable with other platforms.

2. Six good reasons to choose a Partner Digitization Platform

✅ EDI . Only a PDP can enable the exchange of invoices in formats other than the three standard formats: Factur-X, UBL, and CII. 1. The PDP will be responsible for converting the proprietary flow to send it to the administration. This is an advantage for companies that already exchange invoices between themselves in another format, such as EDI (Electronic Data Interchange).

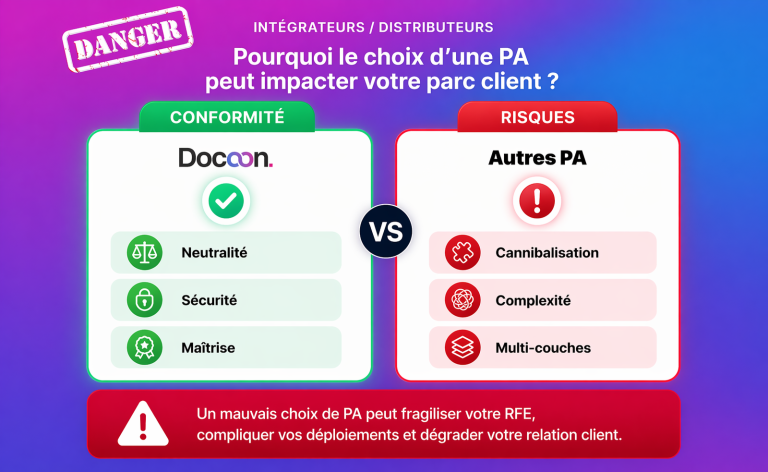

✅Compliance. The very strict specifications that a dematerialization operator must comply with in order to become a Partner Dematerialization Platform ( PDP ) are a guarantee of security and a factor of reassurance. All PDPs must be ISO27001 certified when they apply for registration. They must also provide for data hosting in a SecNumCloud data center. Finally, to be registered as a PDP with the government, operators must pass an audit. In contrast, ODs are not subject to any controls and are not recognized by the government or the tax authorities.

✅Registration in the official directory: after verifying their identity and status, only PDPs will be able to register a company directly without going through the public portal. PDPs will thus be able to delegate identity verification to third parties (accountants, banks, etc.) and facilitate the registration of the 6.8 million companies subject to VAT.

Resilience: In the event of a malfunction of the public billing portal, PDPs will still be able to exchange invoices with each other.

✅International: The network that will be used to comply with the interoperability requirement between PDPs will be the PEPPOL network. This is an expanding international network that is already present in 41 countries. It should also be noted that the security requirements for becoming a Peppol access point will increase. PDPs, which are already subject to ISO 27001 compliance requirements, will already be ready...

✅Additional services such as Order-X 2 : subject to an interoperability requirement for invoices, PDPs will be able to capitalize on this work to exchange other flows such as purchase orders. PDPs will democratize the flows currently processed by EDI 3 for all companies.

At a time when the risk of sensitive data being stolen from a company is ever-present, working with a Partner Dematerialization Platform (PDP) is an objective guarantee of reassurance. Partner Dematerialization Platforms are designed to transmit all mandatory data to the tax authorities on behalf of the companies they support in the electronic invoicing reform. This is why they are required to comply with strict specifications that are subject to audit.

In addition, PDPs will have developed such a high level of compliance and security that they will be best placed to interconnect and exchange data with international platforms: something many companies have been waiting for!

(1) The decree of October 7, 2022, relating to the widespread use of electronic invoicing in transactions between parties subject to value-added tax and the transmission of transaction data states that: partner dematerialization platform operators and the public invoicing portal are required to transmit the electronic invoices referred to in Article 289 bis of the General Tax Code in at least one of the following three formats:

a) The Cross Industry Invoice (CII) exchange standard, developed by the United Nations Centre for Trade Facilitation and Electronic Business (UN/CEFACT);

b) The Universal Business Language (UBL) standard;

c) A mixed format standard consisting of a structured data file in XML format (CII16b) and a PDF file (PDF/A3 standard) (...) This corresponds to the Factur-X format.

(2) Order-X is an electronic order template in a hybrid format built on the same model as electronic invoices in Factur-X format.

(3) Electronic data interchange (EDI) allows not only invoices to be exchanged, but also commercial documents such as purchase orders.