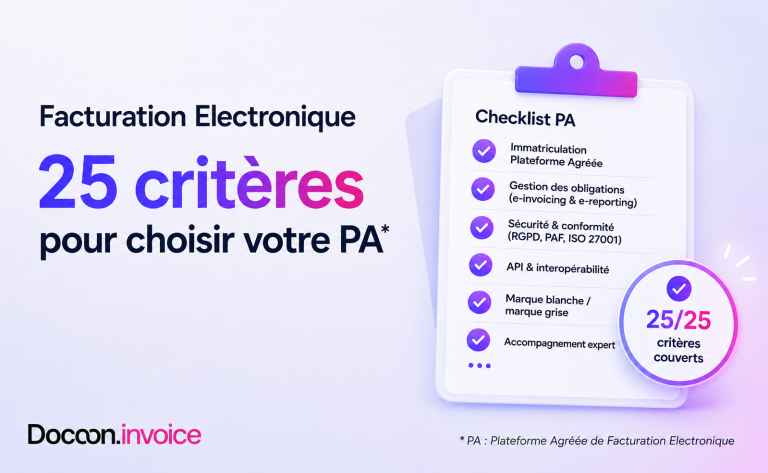

Download your free checklist at the bottom of the article!

Since January 1, 2021, companies have been required to submit their invoices to the public sector electronically. To do so, they use the Chorus Pro portal. The law is changing, as Article 26 of the amended finance law for 2022 provides for mandatory electronic invoicing in transactions between VAT-registered companies established in France. It is important to anticipate this major change now.

As an expert in electronic invoicing, Docoon is naturally committed to providing its partners and customers with a secure and sustainable solution. This article is intended for anyone who still has questions about the scope of the reform and the steps involved. To summarize the issue, below the article you will find an infographic dedicated to the Order To Cash process (customer cycle) that we hope will be both educational and concise. For further information, we also invite you to download our free white paper on the electronic invoicing reform.

1. A transition to prepare for the company

Why is it necessary to prepare for the transition to electronic invoicing now? The law provides for a gradual timetable for implementing the reform, depending on the size of the companies. However, all companies, regardless of their size, must be able to receive invoices in electronic format by July 1, 2024, before gradually issuing them until 2026.

Please note:Sincethis article was written, lawmakers have confirmed two major changes to the reform:

👉 The schedule has been adjusted as follows:

As of September 1, 2026, all companies will be required to accept electronic invoices.

As of September 1, 2026, large companies and medium-sized companies (ETIs) will be required to issue electronic invoices.

As of September 1, 2027, small and medium-sized enterprises (SMEs) and micro-enterprises will be required to issue electronic invoices.

👉 On October 15, 2024, the government announced a significant reduction in the scope of the PPF (Public Invoicing Portal). This public platform, initially designed to issue, receive, and manage electronic invoices for businesses, will now focus solely on two functions: the business directory and the tax data hub for e-reporting. As a result, all companies will now have to turn to a Partner Dematerialization Platform (PDP) to exchange their invoices and report VAT.

As a publisher of digital trust and dematerialization solutions, we strongly advise companies and their partners to anticipate the reform, as it disrupts usual organizational processes and impacts information systems. For a company, anticipating the reform means:

- Organize a team around a project leader to support the implementation of the project.

- Collect all necessary information

- Assess and measure the human and technological requirements to be implemented

- Identify investment needs (equipment and training)

- Select a partner platform

- Consult your usual accounting and management service providers.

- Organize the project with your service provider, publisher, or integrator, or directly with the partner platform.

2. Choosing a partner platform

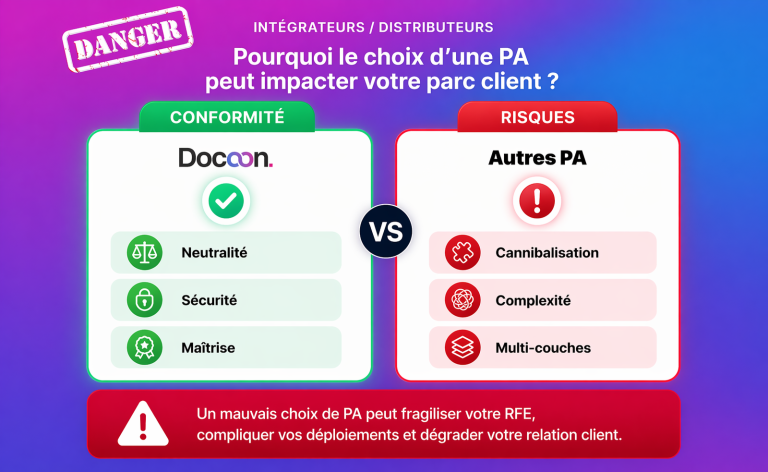

The French legislature has opted for a "Y" model. In practical terms, this means that companies and their technical partners can use Partner Dematerialization Platforms (PDPs) to send electronic invoices to recipients without going through the public invoicing portal, Chorus Pro. These platforms will be registered by the tax authorities. PDPs offer numerous advantages:

- They make the system more resilient.

- They enable companies to maintain existing flows (EDI flows).

They promote innovation by allowing operators to offer an alternative to the public billing portal. PDPs will offer innovative solutions for identifying and authenticating businesses or offering additional services.

This choice is strategic for the company at a time when data security, confidentiality, and archiving have become a priority for IT departments and administrative and financial departments. It should be noted that Partner Dematerialization Platforms are designed to transmit all mandatory data to the tax authorities on behalf of the companies they support in the electronic invoicing reform. This obligation has led the legislator to require them to comply with extremely demanding specifications, which are subject to audit.

While the government allows companies the freedom to organize electronic invoicing with a PDP, a company may also choose to use a Dematerialization Operator (OD). However, an OD is not registered with the tax authorities and cannot issue invoices directly to recipients: it must rely on a PDP or the Public Invoicing Portal (PPF). Consequently, an OD only acts as an intermediary in the electronic invoicing process.

White papers and infographics to download

- The accountant's 5-step checklist

- How to switch to electronic billing